Expertise & Collaboration

Independent, curious thinking drives our team. Each member contributes as a research analyst and has a voice, helping to build group knowledge and insights.

Location: Hong Kong and London, UK

Head of Team: Damian Bird, Portfolio Manager & Analyst

Our Investment Philosophy

High-Quality Growth Companies

Concentrated Portfolios

Long-Term Horizon

Independent Mindset

APPROACH

Our Strategic Approach

Emerging Markets Growth Stock Selection Process

We invest independently of benchmark allocations, seeking companies with difficult-to-replicate competitive advantages. With a business-owner’s mindset, we conduct deep, on-the-ground due diligence to identify attractive investment opportunities. We focus on themes of domestic consumption, economic catch-up, and digitalization—all in pursuit of growth and long-term staying power.

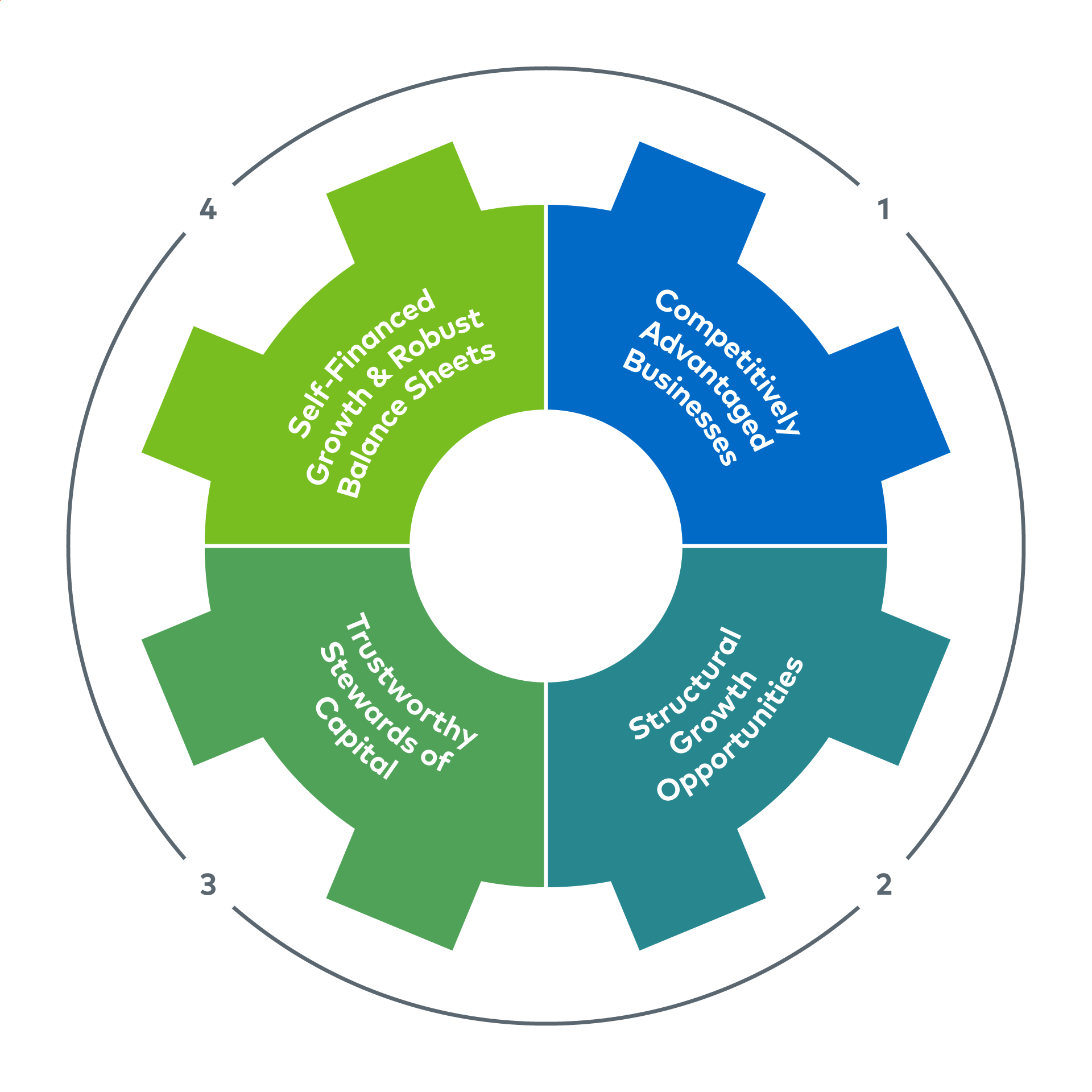

The Compounding Machine

Competitively Advantaged Businesses

- Wide and sustainable competitive moats

- High return on invested capital (ROIC)

Structural Growth Opportunities

- Long term growth runway

- Opportunities to continuously reinvest capital at high rates of return

Trustworthy Stewards of Capital

- Strategically focused management

- Aligned with shareholder interests

- Robust track record of capital allocation

Self-Financed Growth & Robust Balance Sheets

- Attractive cash flows

- Not reliant on external debt or equity financing

There is no guarantee that companies included in the Portfolio will exhibit all of these qualities. This information is not intended to be construed to equate to the expected or projected future performance/returns of a Polen Capital investment or portfolio.

The Polen Emerging Markets Growth strategies typically hold 25 to 40 companies that the portfolio management team feels are the highest-quality growth names. Examples as of 12/31/2024 include:

Tencent Music Entertainment is a leading online music platform in China. With three streaming platforms targeting different demographics, TME has attracted over 578 million monthly active users since its establishment in 2016. In our view, it is a competitively advantaged business that is highly cash-generative with attractive profit margins. We believe revenue and profit growth should come as subscription rates rise and with the addition of ancillary services.

E-Ink is a global leader in Electronic Paper Displays, headquartered in Taiwan. The company's high-quality technology has secured its dominance in electronic paper displays and shelf labels. We believe E-Ink has the potential to compound its earnings at attractive rates over the coming years due to product innovation and increased global adoption of the technology driven by several structural trends, while high barriers to entry protect it from competition.

These stocks were selected as representative holdings due to their large relative size in our Portfolios at the time of selection and their alignment with our investment philosophy.

An Experienced, Research-Driven Team

Investing in emerging markets requires a long-term framework. It is over many years that billions will escape from poverty, cities will rise to the sky, and corporate champions will develop.

Featured

Recent Perspectives

Thought CapitalPolen’s China experts put the recent dramatic market moves into context.

Strategies

Polen Capital Management, LLC is an independent registered investment advisor.

The information is provided for illustrative purposes only. Opinions and views expressed constitute the judgment of Polen Capital as of the period indicated , may involve a number of assumptions and estimates which are not guaranteed, and are subject to change without update. Although the information and any opinions or views given have been obtained from or based on sources believed to be reliable, no warranty or representation is made as to their correctness, completeness or accuracy. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without update, including any forward-looking estimates or statements which are based on certain expectations and assumptions. The views and strategies described may not be suitable for all clients. This information does not identify all the risks (direct or indirect) or other considerations which might be material to you when entering any financial transaction.

Holdings are subject to change. The holdings, as well as other data, are as of the period indicated and should not be considered as a recommendation to purchase, hold or sell any particular security. There is no assurance that any of the securities noted will remain in a portfolio at the time you review this information. Actual holding and percentage allocation in individual client portfolios may vary and are subject to change. The securities discussed do not necessarily represent the entire portfolio. It should not be assumed that any of the holdings discussed were or will prove to be profitable or that the investment recommendations or decisions we make in the future will be profitable. A list of all securities held in this portfolio in the prior year is available upon request. Past performance does not guarantee future results and profitable results cannot be guaranteed.

Absolute Return: is the percent amount that an asset rises or declines in value in a given period. Active Share: is a measure of the percentage of stock holdings in a manager’s portfolio that differs from the benchmark index. Excess Return: returns achieved above and beyond the return of a benchmark.